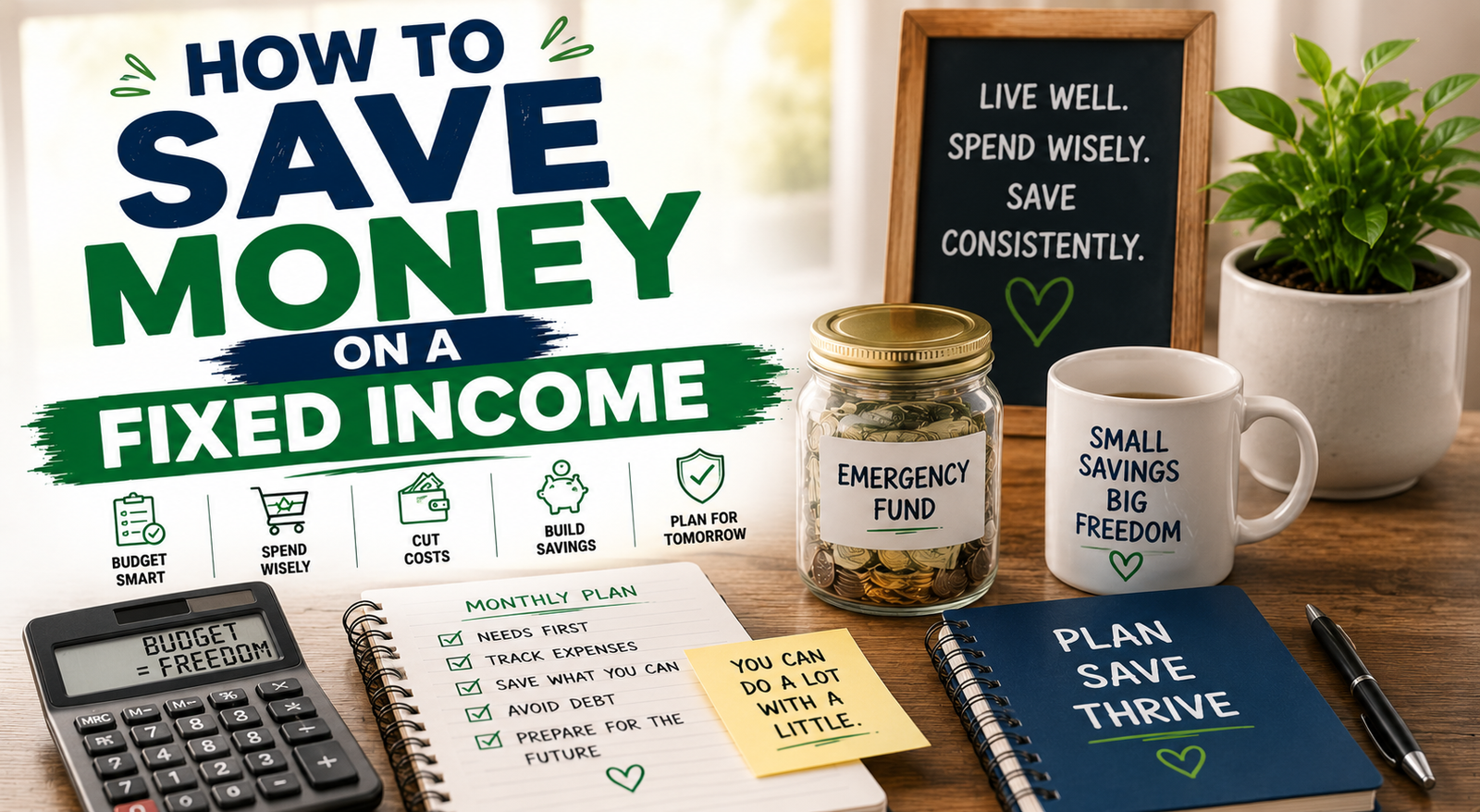

7 Powerful Strategies: How to Save Money on a Fixed Income

For those on a fixed income, it can be difficult to afford the cost of living, particularly with the cost of housing, food, healthcare and utilities on the rise. If you’re receiving retirement benefits, a pension, disability payments or another regular income stream, then careful money management is key. The question that many have is how to make their fixed income dollars last while enjoying the things they need and enjoy in life.

Fortunately, saving money isn’t all about earning more. Financial tweaks can often make a significant difference in the long term. With a bit of financial savvy, it’s possible to establish financial security even with modest income, by making smart spending choices and focusing on essential expenses.

Why is it important to save on a fixed-income?

If your income doesn’t fluctuate drastically from one month to the next, you can find yourself facing financial hardship if you suddenly have unplanned costs.

Here are some of the reasons why it’s important to save money:

- Greater financial security

- Better emergency preparedness

- Reduced financial anxiety

- Greater flexibility with your budget.

- Insurance to guard against increases in the cost of living.

Small savings can add up over time.

Identify your financial situation

Saving money is the first step, knowing where your money goes is the first.

Many are shocked to review their expenses for an entire month and how much money is being spent on unnecessary items.

Review:

- Housing costs

- Utilities

- Groceries

- Transportation

- Insurance

- Healthcare

- Entertainment

An understanding of how much you spend can help you find places to save money.

Strategy 1 – Make a realistic budget

One of the best methods for handling a set sum of earnings is a budget.

Rather than trying to make a plan too limiting, try to think about establishing a budget that is consistent with your true life and requirements.

The elements of a practical budget should:

- Pay off all essentials first

- Include savings contributions

- Eat or drink, just a little from time to time!

- Get ready for unforeseen expenses:

An aggressive budget will not succeed whereas a realistic budget will.

Strategy 2. Reduce Monthly Utility Costs

Electricity and gas bills can be a significant expense.

There are some simple tweaks that can cut costs:

- Turn off unused lights

- Use energy-efficient appliances

- Seal around doors and windows.

- Reduce water waste

- Control heating and air conditioning temperatures

While these changes might be simple and insignificant on their own, they can add up and bring down monthly costs.

Strategy 3: Save Money on Food

Consequently, depending on fixed income, food costs can easily take up a significant portion of the budget.

Try these ways of saving money:

- Eat according to a schedule

- When shopping, carry a shopping list.

- Buy store brands

- Compare prices

- Reduce food waste

Plan meals, particularly for families, and cut costs while eating a healthy diet.

Strategy 4 : Eliminate Unnecessary Subscriptions

If you have subscriptions to other publications and magazines, cancel them.

A lot of people spend money on services that they don’t use often.

Go through the monthly bills and examine the following monthly costs:

- Streaming services

- Memberships

- Mobile apps

- Software subscriptions

Services that are not being used can be cancelled to make room for savings or for services that are needed.

Strategy 5: Build up an Emergency Fund

Unexpected expenses are unavoidable.

Examples include:

- Medical bills

- Home repairs

- Vehicle maintenance

- Appliance replacements

Making even small savings in an emergency fund can be helpful if something unexpected happens.

It’s not just about the quantity of savings but also the consistency.

Strategy 6: Take Advantage of Discounts and Assistance Programs

There are many discount plans available that are geared toward individuals who have a fixed income.

Some areas for potential savings are:

- Utility assistance programs

- Prescription discounts

- Senior discounts

- Community services

- Transportation discounts

Completing the research on the programs available in your area could result in valuable savings.

Strategy 7: Needs before wants

One of the best financial practices is to differentiate between needs and wants.

Needs include:

- Housing

- Food

- Healthcare

- Transportation

- Utilities

Wants may include:

- Luxury purchases

- Frequent dining out

- Impulse shopping

- Premium subscriptions

This leaves you with a stable financial situation, while prioritising essential expenses.

Common challenges that people with a fixed income may face

Financial pressures can be different for individuals on a fixed income.

Inflation

Over time the purchasing power decreases as prices increase.

Healthcare Costs

The cost of medical care may rise out of the blue.

Limited Income Growth

Generally, the growth of fixed incomes is not as fast as the growth of living expenses.

Emergency Expenses

Unpredictable expenses can derail well laid plans.

Acknowledging these challenges will help to prepare financially.

Small savings go a long way!

Many think that one needs a lot of money to save.

However, small contributions will add up.

For example:

- Saving little by little week after week

- One of the unnecessary expenses is reduced.

- Lowering utility bills

- Avoiding impulse purchases

These practices can make a significant contribution to your financial success over months and years.

Steps to build a LTSM mentality

Success in saving isn’t so much about how much money you have, it’s about how much you put into the bank.

Focus on:

- Tracking expenses

- Following a budget

- Building healthy habits

- Avoiding unnecessary debt

- Saving regularly

These behaviors can foster financial stability, no matter how much money you make.

Final Thoughts

Saving money on a fixed income is all about making calculated financial choices and ensuring that you make the best out of every dollar. While a fixed income can come with its own set of difficulties, it is possible to structure a budget in an effective way, make careful spending choices, and make regular savings efforts to achieve a more stable and peaceful lifestyle.

The idea isn’t perfect perfection. Rather, take it one step at a time and strengthen your finances over time. Virtually any savings amount can offer much protection and comfort in the years ahead.

FAQS

Is there an opportunity to reduce expenses on a fixed income?

Yes. With a fixed income, one can save money in a number of ways, including careful budgeting, cutting unnecessary expenses, and establishing a consistent savings regimen.

Which is the optimal budgeting strategy for an income that is fixed?

An easy budget that focuses on what is needed, what will be saved and what an emergency fund will be used for is usually the best strategy.

What is the monthly savings amount?

This will depend on the individual’s situation. It’s more important to be consistent than the exact quantity.

Why is it necessary to have an emergency fund if you have a fixed income?

An emergency savings fund is a type of saving that can be used to pay for emergencies without borrowing money.

Which costs are to be cut first?

Often it’s a good idea to start by eliminating non-essential subscriptions, impulse purchases, and discretionary spending that could have been avoided.