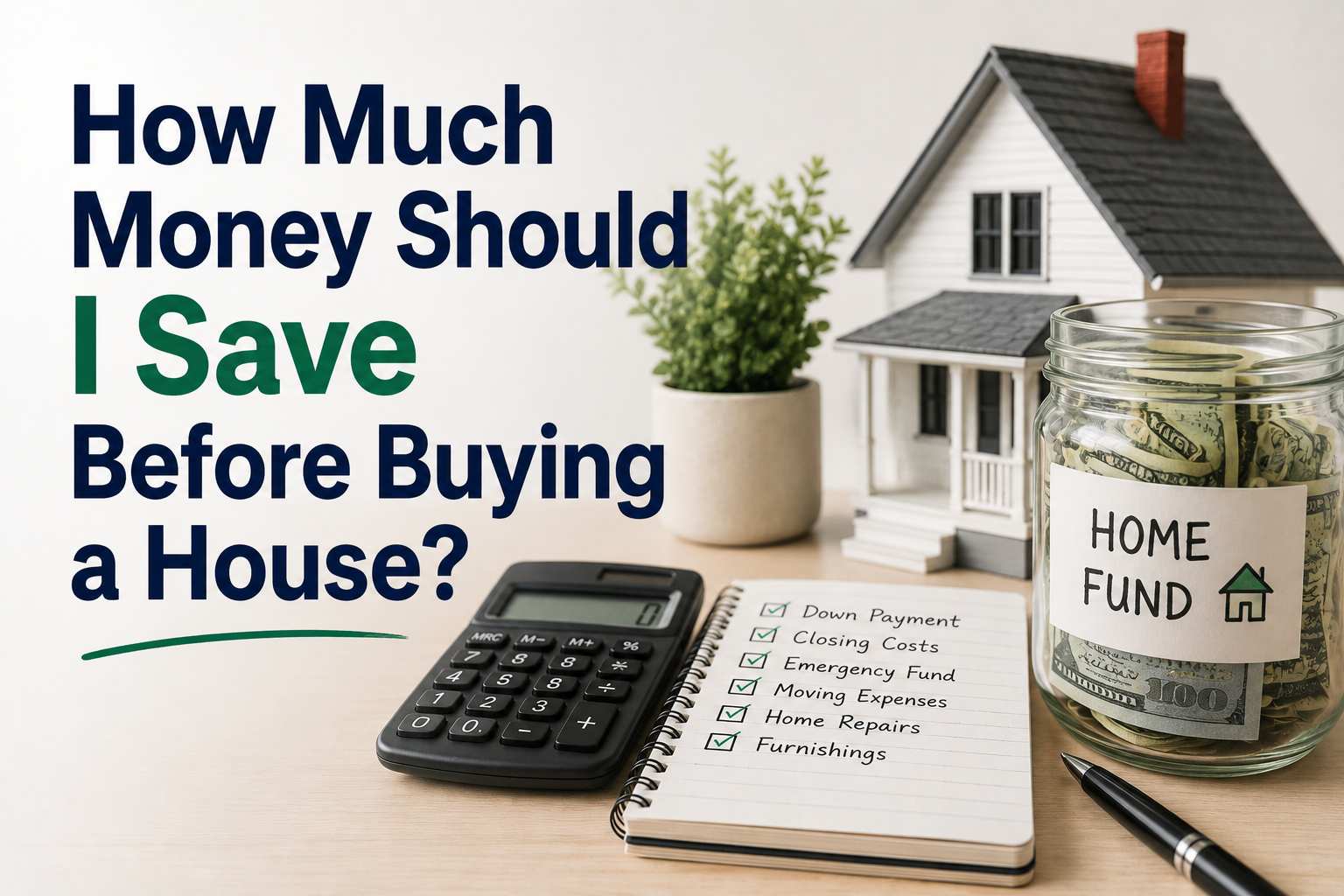

9 Smart Savings Goals: How Much Money Should I Save Before Buying a House?

Purchasing a home is among the greatest monetary choices that most will make. Future homeowners tend to think of their monthly mortgage payments but the costs associated with buying a home are generally bigger than what they think. This makes many buyers wonder about an important question: How much of a budget should I save before purchasing a home?

It will depend on your income, the cost of the home, the type of mortgage you have and your finances. When it comes to saving for a home, it’s not just about the down payment. Other things to consider are closing costs, moving costs, emergency repairs, and other home maintenance costs.

A solid savings plan can help keep the home buying process smoother and prevent financial stress after you move in.

Why do saving before buying a house matter?

Many would focus all on getting approved for a mortgage. But there are also a number of closing costs and prepaid items associated with purchasing a home.

Good saving will enable you to:

- Reduce borrowing costs

- Reduce monthly mortgage payments

- Boost your likelihood of getting loans approved

- Cover unexpected expenses

- Build financial confidence

- Avoid becoming house-poor

Having financial preparation is a huge benefit when it comes to enjoying homeownership.

1. Saving for a down payment

One of the biggest costs involved with buying a home is often the down payment.

The typical buyer’s expectation has been to pay 20 percent down. There are some mortgage programs that require less down payment based on lender specifications, though.

For example:

- 3% down on a $300,000 home = $9,000

- 10% down on a $300,000 home = $30,000

- 20% down on a $300,000 home = $60,000

Making a larger down payment can lower your monthly payments and possibly result in more favorable loan terms.

2. Set up for Closing Costs

Many first time buyers don’t realize what the closing costs will be.

Closing costs may consist of:

- Loan origination fees

- Appraisal fees

- Title insurance

- Attorney fees

- Property taxes

- Recording fees

This cost is typically due at closing and can cost thousands of dollars to buy a home.

Stashing aside cash for closing costs can avoid unpleasant surprises.

3. Make a supply of emergency money

Purchase of a home should not be all your savings.

There are some unexpected costs associated with homeownership, including:

- Roof repairs

- Plumbing issues

- HVAC repairs

- Appliance replacements

- Water damage

When unforeseen repairs need to be made, an emergency fund will come to the rescue.

After buying their home, many financial experts recommend keeping several months of living expenses.

4. Save for Moving Expenses

The cost of moving can easily add up.

Potential expenses include:

- Moving trucks

- Professional movers

- Packing supplies

- Utility deposits

- Furniture transportation

Local moves can come more expensive than you think.

If you plan for moving, you don’t have to rush and deal with an unexpected move.

6. Forecast Home Maintenance Expenses

All houses need continuous maintenance.

Common expenses include:

- Lawn care

- Painting

- Gutter cleaning

- Pest control

- Minor repairs

The concept is to save money annually for maintenance and upkeep.

Maintenance cost is a cost that if not addressed now, will cause bigger and costlier issues later on.

6. Take into account Property Taxes and Insurance

Often, mortgage payments consist of more than the mortgage itself.

Homeowners can also pay:

- Property taxes

- Homeowners insurance

- Mortgage insurance (if applicable)

When buying a home, these are ongoing costs which you should consider in your budget.

If you know the total cost of ownership, you’ll know what it will take to save more money.

7. Avoid Becoming House-Poor

If you are approved for a big mortgage, it doesn’t mean that you have to borrow the highest amount.

When a person saves too little and spends too much on housing, he or she can easily find him or herself in financial trouble.

Saving more before purchase can offer:

- Greater flexibility

- Lower monthly payments

- Better financial security

- Reduced stress

Your home should enhance your lifestyle, not place a constant burden on your finances.

8. Strengthen Your Credit and Savings Together

In addition to saving for a house, it’s crucial to enhance your financial profile.

Lenders often evaluate:

- Credit scores

- Debt levels

- Income stability

- Savings history

Having a better financial standing can possibly help you to receive the best mortgage rates and the lowest repayments at the time of borrowing.

With your savings and the proper management of credit, you can have a considerable increase in your purchasing power.

9. Set a customized savings goal

It’s not a hard and fast rule that every home buyer will need to save a specific amount.

Target will vary based on:

- The value of your house or apartment in your area.

- Income level

- Mortgage type

- Existing debts

- Personal financial goals

By designing a personalized savings plan, you can get a more solid start on home ownership.

The optimal savings plan is one that will help to buy something and maintain a good financial position in the future.

What is the amount of savings that should be made by first-time buyers?

One of the advantages for first-time home buyers is to have more than one savings objective, rather than just the down payment.

Common savings plans might include:

- Down payment fund

- Closing cost fund

- Emergency savings

- Moving expenses

- Initial maintenance reserve

Separate categories may give you a better idea of your readiness to purchase.

Common mistakes that home buyers make

One of the most common reasons for financial problems among many buyers is that they don’t account for all the costs of homeownership.

Common mistakes include:

The down payment used was All Savings

Without an emergency reserve, you could be financially vulnerable.

Ignoring Closing Costs

When purchasing a home, many buyers consider only the mortgage and ignore closing costs.

Underestimating Repairs

Unexpected maintenance may be needed in even newer homes.

Mortgages for more house than they can afford

This may actually decrease financial flexibility due to increased mortgage payments.

Skipping Financial Planning

The long-term success is enhanced by a comprehensive savings strategy.

There are some indications that you may be ready to buy a house

If you are financially prepared, then:

- You have a stable income

- You’ve made a down payment.

- Closing costs can be financed.Closing costs are payable in installments.

- You have an emergency savings account.

- You have a manageable debt load

- You will be residing in the area for a few years.

These indicators tend to offer more evidence of homeowner readiness.

Conclusion

If that is the case, how much should I save before I purchase a house? It’s not just about putting money into savings for a down payment. Other closing costs, moving costs, maintenance, emergency repairs, taxes and insurance are also costs for the future home-buyer.

Making it more affordable and less stressful to own a home can be achieved with a well-planned savings strategy. Finishing several savings accounts and practising good financial habits can help you feel more at ease and secure about buying a house.

FAQS

What should be my home saving target?

There are several expenses to save for when purchasing a home, including the down payment, closing costs, moving costs, emergency savings, and future maintenance costs.

Do you need to pay a down payment of 20%?

Not always. Some mortgage loan packages have the ability to accept smaller down payments, but this depends on the lender.

But should I continue to save after I purchase a home?

Yes. Having an emergency fund means you have money available to pay for unexpected repairs or emergencies.

What is included in closing costs purchased?

Lender costs, title costs, appraisal costs, taxes, and other transaction costs can be included in closing costs.

What is the best way to determine if I have the money to purchase a home?

Financial readiness may be identified by stable income, manageable debt, adequate savings, and having emergency reserves.